Search, Compare, Save

Instant quotes, incredible prices, insurance everywhere

10,000+

30%

Clients Served

Average Client Savings

88,234

Insurance Plans Available

5 Star Rated

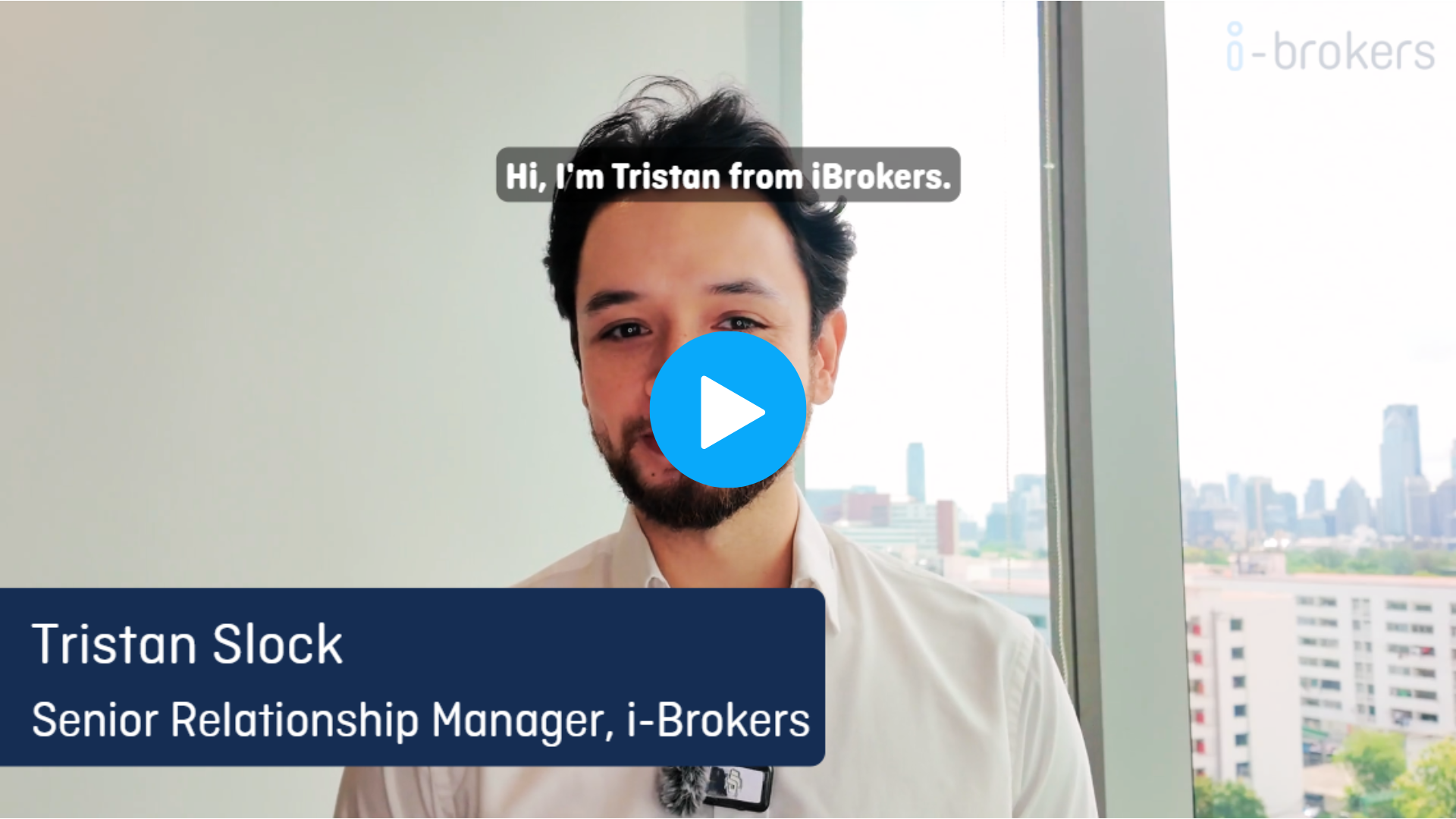

At i-Brokers, our goal is to ensure that each and every one of our customers has a wonderful experience. We are pleased to have earned excellent ratings from many who we have served and aim to exceed these standards every day.

How It Works

i-Brokers are passionate about insurance and finding the best possible prices for our customers. We do this by working closely with insurance companies across the world.

Step 1: Search

Tell us what kind of insurance you need and we’ll do the rest. Everyone’s situation is different, so just share a few details and we’ll start matching you with the right plans.

Step 2: Compare

We’ll show you a personalised list of plans that fit your needs. Easily compare benefits, pricing, and customer ratings, all in one place, with no hidden surprises.

Step 3: Save

82% of our customers save money on premiums by switching their plans through i-Brokers. It only takes a few minutes, and the savings could be well worth it.

What Our Clients Say

Our Latest News